Time trading strategies

Contents:

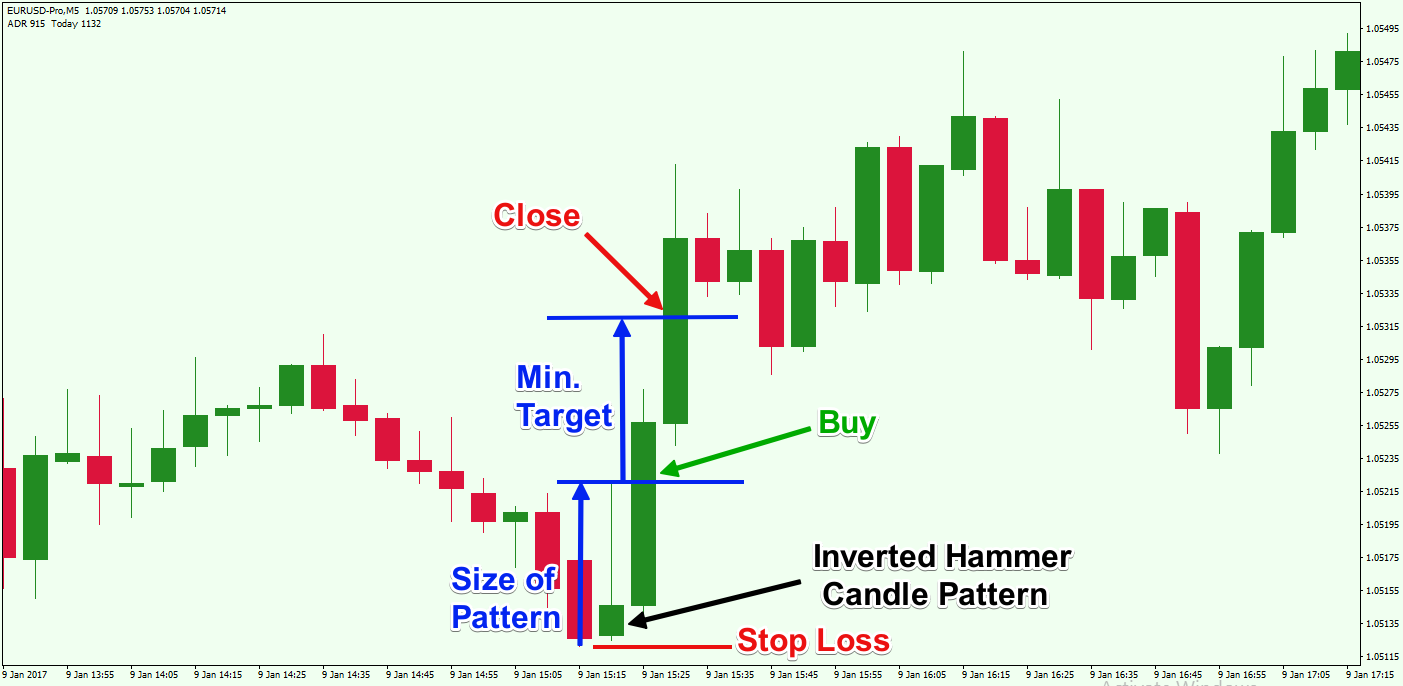

Additionally, there is the RSI to make sure the signals provided by the system are very powerful. It will filter the fake signals and leave the valuable ones. You can use it in any time frame. You can trade using 1m, 5m, 15m, or higher chart time frame.

START TRADING IN 10 MINUTES

Choose the one you are comfortable with. Three indicators work together and you must watch all of them. Before entering the trade make sure all the conditions are met. And what are the conditions for opening a long position? You can hold the position open for as long as the chart time frame multiplied by 5. With a 1-hour chart, you can keep the position open for 5 hours. With a 5-minute time frame, you can keep it around 25 minutes. The strategy described today can be used in various markets.

Moreover, using it is quite simple. Nevertheless, the signals provided are really powerful.

I can spend all the times in trading. I am trying to return to trade again after 5 years of rest and currently studying the market to set up my trading plan. Several possibilities present themselves to develop this strategy further. Am a day trader. Initially, the trader must spend time tracking the markets and evaluating market forces before committing to a trade, but can then take a step back as they ride out market movements for an extended time. Before entering the trade make sure all the conditions are met. Start trading on a demo account.

Naturally, you have to always check whether all conditions are fulfilled. It can generate constant profits from trading the trends. There are three indicators involved and you need to watch all of them. It requires a great portion of patience and concentration. You need to observe the chart, sometimes for a long time, before the favorable situation occurs. Many professional traders believe that trend trading strategies are the most valuable ones. Today, you got to know one of such systems that combines three indicators.

You should always protect your capital and you can do it by applying money management strategies as well as having emotions under control. Taking time to learn these skills will minimize the risk of losing money and improve your chances of conducting profitable trades. Use the Olymp Trade demo account before you begin investing real money. Keep in mind that these strategies are not guarantees for earning, as no strategy is completely risk-free.

Therefore, always be prepared to deal with losses. I would be happy to hear from you. Average rating 4.

- 3. Swing trading strategy?

- Introduction;

- Trading strategy: 1-Minute Breaks.

- how to make money trading forex;

Vote count: No votes so far! Be the first to rate this post. Your email address will not be published.

- how do banks trade in forex;

- Reader Interactions;

- forex commodity pairs?

- Top 3 Brokers Suited To Strategy Based Trading.

Having a solid trading strategy is a key point in your way to becoming successful in trading. You … [Read More The morning star candlestick pattern is the perfect indicator of the lowest point of the downtrend. Many traders will start from a demo account. And this is, in fact, a very good idea.

You can learn a … [Read More The Olymp Trade platform develops constantly to satisfy its clients' expectations. New … [Read More How to use new subscription based services?

Olymp Trade security requirements demand that you enter your account details, this means the email … [Read More Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website.

Assuming the lack of complete information, randomness plays a key role, since efficiency is impossible to be reached. This is particularly important in order to underline that our approach does not rely on any form of the above mentioned Efficient Markets Hypothesis paradigm. More precisely, we are seeking for the answer to the following question: if a trader assumes the lack of complete information through all the market i.

Instead, a complex network of self-influencing behavior, due to asymmetric circulation of information, develops its links and generates herd behaviors to follow some signals whose credibility is accepted. Financial crises show that financial markets are not immune to failures. Their periodic success is not free of charge : catastrophic events burn enormous values in dollars and the economic systems in severe danger.

Trading Strategies

Are traders so sure that elaborated strategies fit the dynamics of the markets? Rational expectations theorists would immediately bet that the random strategy would loose the competition as it is not making use of any information but, as we will show, our results are quite surprising. We consider four very popular indexes of financial markets and in particular, we analyze the following corresponding time series, shown in Fig. See text for further details.

In general, the possibility to predict financial time series has been stimulated by the finding of some kind of persistent behavior in some of them [38] , [54] , [55]. The main purpose of the present section is to investigate the possible presence of correlations in the previous four financial series of European and US stock market all share indexes. In this connection, we will calculate the time-dependent Hurst exponent by using the detrended moving average DMA technique [56].

Let us begin with a summary of the DMA algorithm. The computational procedure is based on the calculation of the standard deviation along a given time series defined as. In order to determine the Hurst exponent , the function is calculated for increasing values of inside the interval , being the length of the time series, and the obtained values are reported as a function of on a log-log plot. In general, exhibits a power-law dependence with exponent , i. In particular, if , one has a negative correlation or anti-persistent behavior, while if one has a positive correlation or persistent behavior.

The case of corresponds to an uncorrelated Brownian process. In our case, as a first step, we calculated the Hurst exponent considering the complete series.

This analysis is illustrated in the four plots of Fig. Here, a linear fit to the log-log plots reveals that all the values of the Hurst index H obtained in this way for the time series studied are, on average, very close to 0. This result seems to indicate an absence of correlations on large time scales and a consistence with a random process. The power law behavior of the DMA standard deviation allows to derive an Hurst index that, in all the four cases, oscillates around 0. See text. On the other hand, it is interesting to calculate the Hurst exponent locally in time.

In order to perform this analysis, we consider subsets of the complete series by means of sliding windows of size , which move along the series with time step. This means that, at each time , we calculate the inside the sliding window by changing with in Eq.

Hence, following the same procedure described above, a sequence of Hurst exponent values is obtained as function of time. In Fig. In this case, the values obtained for the Hurst exponent differ very much locally from 0.

Strategies for Fixed Time Trading on Olymp Trade - Official Olymp Trade Blog

This investigation, which is in line with what was found previously in Ref. As we will see in the next sections, this feature will affect the performances of the trading strategies considered. In the present study we consider five trading strategies defined as follows:. Then, if , the trader predicts an increment of the closing index for the next day i. In the following simulations we will consider days, since this is one of the most used time lag for the momentum indicator.

See Ref. A divergence can be defined referring to a comparison between the original data series and the generated RSI-series, and it is the most significant trading signal delivered by any oscillator-style indicator. It is the case when the significant trend between two local extrema shown by the RSI trend is oriented in the opposite direction to the significant trend between two extrema in the same time lag shown by the original series. When the RSI line slopes differently from the original series line, a divergence occurs.

Look at the example in Fig. In the case shown, the analyst will interpret this divergence as a bullish expectation since the RSI oscillator diverges from the original series: it starts increasing when the original series is still decreasing. In our simplified model, the presence of such a divergence translates into a change in the prediction of the sign, depending on the bullish or bearish trend of the previous days.

In the following simulations we will choose days, since - again - this value is one of the mostly used in RSI-based actual trading strategies. A divergence is a disagreement between the indicator RSI and the underlying price. By means of trend-lines, the analyst check that slopes of both series agree. When the divergence occurs, an inversion of the price dynamic is expected.

In the example a bullish period is expected. This deterministic strategy does not come from technical analysis. If, e. In any moment t ,. In particular, the first is the Exponential Moving Average of taken over twelve days, whereas the second refers to twenty-six days. The calculation of these EMAs on a pre-determined time lag, x , given a proportionality weight , is executed by the following recursive formula: with , where.

What is the best Forex trading strategy?

Once the MACD series has been calculated, its 9-days Exponential Moving Average is obtained and, finally, the trading strategy for the market dynamics prediction can be defined: the expectation for the market is bullish bearish if. In this connection we are only interested in evaluating the percentage of wins achieved by each strategy, assuming that - at every time step - the traders perfectly know the past history of the indexes but do not possess any other information and can neither exert any influence on the market, nor receive any information about future moves.

In the following, we test the performance of the five strategies by dividing each of the four time series into a sequence of trading windows of equal size in days and evaluating the average percentage of wins for each strategy inside each window while the traders move along the series day by day, from to.

This procedure, when applied for , allows us to explore the performance of the various strategies for several time scales ranging, approximatively, from months to years. The motivation behind this choice is connected to the fact that the time evolution of each index clearly alternates between calm and volatile periods, which at a finer resolution would reveal a further, self-similar, alternation of intermittent and regular behavior over smaller time scales, a characteristic feature of turbulent financial markets [35] , [36] , [38] , [58].

Such a feature makes any long-term prediction of their behavior very difficult or even impossible with instruments of standard financial analysis. The point is that, due to the presence of correlations over small temporal scales as confirmed by the analysis of the time dependent Hurst exponent in Fig.

But this could depend much more on chance than on the real effectiveness of the adopted algorithm. On the other hand, if on a very large temporal scale the financial market time evolution is an uncorrelated Brownian process as indicated by the average Hurst exponent, which result to be around for all the financial time series considered , one might also expect that the performance of the standard trading strategies on a large time scale becomes comparable to random ones.

In fact, this is exactly what we found as explained in the following.