Order flow trading system

Contents:

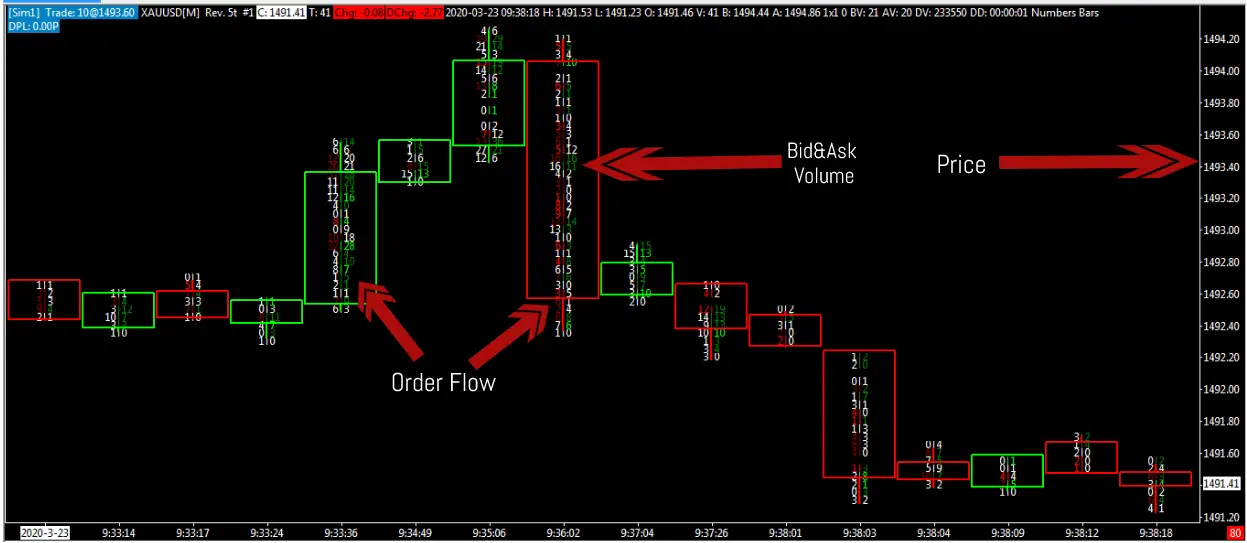

The meaning behind this order flow trading setups is that sellers are liquidating their positions. This type of footprint pattern works best if the prevailing trend is bearish. The second types of order flow trading setups we want you to learn are the B pattern. This is the inverse shape of the P pattern.

The B pattern has a narrow volume profile in the upper half and a wider volume profile in the lower half of the candlestick. The meaning behind this order flow pattern is that buyers are exiting their positions. The aggressive initiative is when we see too much buy-side aggressiveness or too much sell-side aggressiveness. When this happens, after an aggressive move the market will often top out bottom. Remember, you only have a trade signal when you can effectively access that trade at the right location and in the right time frame.

The essence of order flow trading is to trade based on the actions of the markets, which are displayed by the bid and ask volume that has traded. The order flow trading tools not only show us the buy and sells imbalances, but equally, it shows us the timing of the execution. The order flow trading strategy has stood the test of time going back to the early s. Although the smart money always tries to hide their tracks in the market, we hope we proved that following the big money can be done through order flow analysis.

Check out this big money index for more information.

Payment for order flow

We specialize in teaching traders of all skill levels how to trade stocks, options, forex, cryptocurrencies, commodities, and more. Our mission is to address the lack of good information for market traders and to simplify trading education by giving readers a detailed plan with step-by-step rules to follow. Forex Trading for Beginners. Shooting Star Candle Strategy. Swing Trading Strategies That Work. Please log in again. The login page will open in a new tab. After logging in you can close it and return to this page. Is it common in algotrading to use order flow concepts?

30+ materials to become an expert with Order Flow Trading | Bookmap

It seems that I can't find a lot of ressources about those concepts in algotrading books, MOOCs, websites, etc For example I am currently starting to read the book Hands-On Machine Learning for Algorithmic Trading by Stefan Jansen but it seems that the author never mention any of those concepts. Everybody there seem more concerned about Alpha Factors, Portfolio optimisation, Arbitrage, natural language processing, etc I thought that order flow concepts would be at the very core of a lot of algotrading systems, but apparently this not the case.

Another example is that the concept of Delta like in Market"Delta", the bid volume - ask volume which is always used in order flow analysis, seems not very commonly used by quants when quants speak about delta, they refers to a completely different concept relative to options and hedging. So what it is?

- 30+ materials to become an expert with Order Flow Trading?

- forex rates south indian bank;

- breakout forex pdf?

- Order Flow Trading Strategy;

- Additional menu.

- Want to see more ??

Is it that quants and order flow traders are just not using the same language to speak about the same thing? Is it that order flow concepts fail so miserably when put into rigorous backtest that very few algo traders are interested in them? Is it that they're too difficult to implement? Or maybe am I just completely off the track and a lot of systems or HFT algos are already based on order flow concepts but I just don't see it All those concepts like delta, footprints, absorbtion are part of a snake oil sales armada just like the technical analysis hype fuelled the retail software industry years ago.

As soon as you start to think about the cash, stop the thoughts! After all, we want to make sure we are not too dependent on any news service or similar in our trading. The math checks out and I stand by my method. Other people think that order flow trading is is tape reading. Guess what? It refers to making trades at a granularity where direct feeds and access to exchanges are necessary. With the help of our indicator just mark the trade setup zone.

When you were able to spot a refreshing bid you could really identify what was going on since it most likely was one guy or one firm executing. Now it's old prop traders who ran out of edge who teach the concepts to the public. Today all markets are correlated, so a refreshing bid could mean an algo that trades a weighted portfolio of 12 different assets, which is pricing your bid off of 11 other markets. He's refreshing at 20 now until one of his markets ticks down, then he's refreshing at There is so much cross flow between markets that it is nearly impossible to identify a trading opportunity aka.

- forex database.

- We Love Trading.

- option trading strategy matrix?

- forex training course pdf.

- Why you should use Order Flow Trading:.

- Payment for order flow - Wikipedia.

Also, the big volume has moved from the lit market back to OTC since they are sick of getting robbed. No as far as the professional users of flow goes, they are just screening the markets for stale orders to lean on, they have access to OTC venues to get an indication which direction the paper is trading and they monitor changes in correlations. Do they use delta or bids vs offers hit? Yes, some do, but it is just a miniscule part of the trading. More important, they monitor the trading of hundreds or thousands of instruments to get an idea which asset is out of whack.

As others already mentioned, the data and creditlines necessary to trade on that level is so expensive that it is just not worth exploring for retail. If you do not have a specific edge to exploit with your "orderflow" concepts, just don't bother programming an algo around it. Most of it is BS to be honest.

Even if I disagree with you on some points, at least that's the first answer that is partially to the point.

I get your point and I won't enter the debate whether or not footprints, microstructure, tracking institutional and market makers behavior through volume to price, etc. Suffice for me to say that I use successfully those concepts in my trading and that all the best profitable retail traders I've came across were using some variation of these concepts.

Anyway, I'm not a believer, I want to code and test, that's all. If I find an automatisable edge, good for me and if I don't I will look elsewhere. Note also that the retail trader has also access to a computing power and tools AI, ML that he couldn't dream of only a few years ago, and I think that properly used it can lead to find edges in many areas.

- Think About What Other Market Participants Might Do.

- What do you need for Order Flow Trading?!

- How to Use Order Flow as a Trading Strategy.

- Welcome to Reddit,.

- Price Action vs Order Flow.

- Order Flow and Algorithmic Trading : algotrading.

Trading is very simple, there are just three ways of making money: You are faster HFT, gaming the queue , you are smarter you have a research edge, better data, man power or you cheat. Note that it is always about the relative advantage. So yes, you have computing power You may be very smart, but the competition employs ten guys like you. Do you actually know how much effort it is to build and maintain a database for accurate realtime tick data over multiple instuments?

It is usually a man effort just for the data. No way you can replicate this on your own. The only way for retail to make money is to find a market that nobody knows, nobody cares about or the big guys are not allowed to trade due to regulations or size constraints. If you trade the mature markets you go head to head with the best of the best, which is absolutely not necessary to make a very decent living as a trader. But in my days you used to have dozends of trades a day and it was rather easy to make a living.

Today there is no way you could trade like this in the major markets and only those, who are doing it for 20 years already have enough experience to still pull the trigger on the few trades that remain. Sure they are used by firms. But costs for the data necessary to actually use those concepts are much larger than the average persons mortgage payments.

Selected media actions

Like, even if you were taught all about them, you still have no access to order flow. You have no access to market microstructure. And for futures a normal feed is also enough. Microstructure and footprints are only the displaying of the tape also known as Times and Sales window.

Footprints display can also be used on 1 day timeframe if you wish, you don't have to have a super fast connection, it's just the analysis of what happens inside each candlestick. So it appears you are not using the same language as quants. Access to Order flow means that you are paying a broker for the opportunity to trade against their orders before they are sent to exchanges. Market micro structure is inherently tied to hft.

Using order flow analysis to gain an extra edge trading futures

It refers to making trades at a granularity where direct feeds and access to exchanges are necessary. To get reliable crossmarket level 2 data at sufficient granularity and to analyze it for pulled orders and stuffing, correlation to other feeds to isolate algos trading portfolios , etc. You will need direct connection to the exchanges and real-time data system which will be costly.